A Practical Understanding of General Insurance Underwriting and Claims Management is a short 2-day in-person virtual course organised by the Malaysian Insurance Institute, where I learned the gained insights on the workings of underwriting and claims management.

What is it?

A Practical Understanding of General Insurance Underwriting and Claims Management is a short online course organised by the Malaysian Insurance Institute. I attended the 2 day course on 1 – 2 November 2022, thanks to my employer sponsoring my education. The class went on from 9 am – 4 pm with Mr Kwong as the lecturer.

Mr Kwong has a rule in place where our webcams have to be on at all times and he has the tendency to ask students for feedback. His teaching method definitely snowballed my learning experience!

How much does it cost?

EARLY BIRD – MII MEMBER

Single: RM1,080 | USD250

EARLY BIRD – NON MEMBER

Single: RM1,180 | USD272

NORMAL FEE – MII MEMBER

Single: RM1,180 | USD272

Group of 3: RM1,030 | USD240

NORMAL FEE – NON MEMBER

Single: RM1,280 | USD300

Group of 3: RM1,080 | USD250

* Fees inclusive of 6% SST (Malaysia Sales and Service Tax)

I suggest that if you really want to attend this short course, discuss your interest with your manager and get your employer to sponsor you.

What are You Expected to Learn from this Course?

At the end of the course, participants will be able to:

- know what are the fundamentals of underwriting in insurance; and

- list the functions of the overall claims management

Course Content:

- Introduction to underwriting

- Underwriting process

- Underwriting ecology system

- Pricing

- Challenges

- Claims management concepts and procedures

- Outsourcing of claims functions

- Claims estimating and reserving

- Ex gratia and fraudulent claims

- The role of litigation in claim process

- Approaches to complaint handling and dispute resolution

- Bank Negara Malaysia guidelines on Motor and Non Motor Claims

- Case Study

My Top 3 Learnings of General Insurance Underwriting

1. The role of an Underwriter in Assessing a Risk

- Assessing the risk brought to the common pool

- Deciding whether to accept the risk

- If so, at what terms and conditions and how much to accept

- Calculating a suitable premium to be charged

I personally find this lesson the most relevant as I work as an underwriter. It is beneficial to understand that the role of an underwriter is to help insurer manage risk on a case-by-case basis. It helps gives me clarity that what I do at my day job has an impact to the company!

2. 6 Principles of Insurance

- Insurable Interest

- Utmost Good Faith

- Indemnity

- Contribution

- Subrogation

- Proximate Cause

Insurance is a highly-regulated industry, so I find it helpful to know the rights and obligations of both insurers and policyholders, ensuring transparency, fairness, and proper functioning of insurance contracts, thereby facilitating effective risk management and dispute resolution in the event of losses.

Check out my article on the 6 Basic Principles of Insurance!

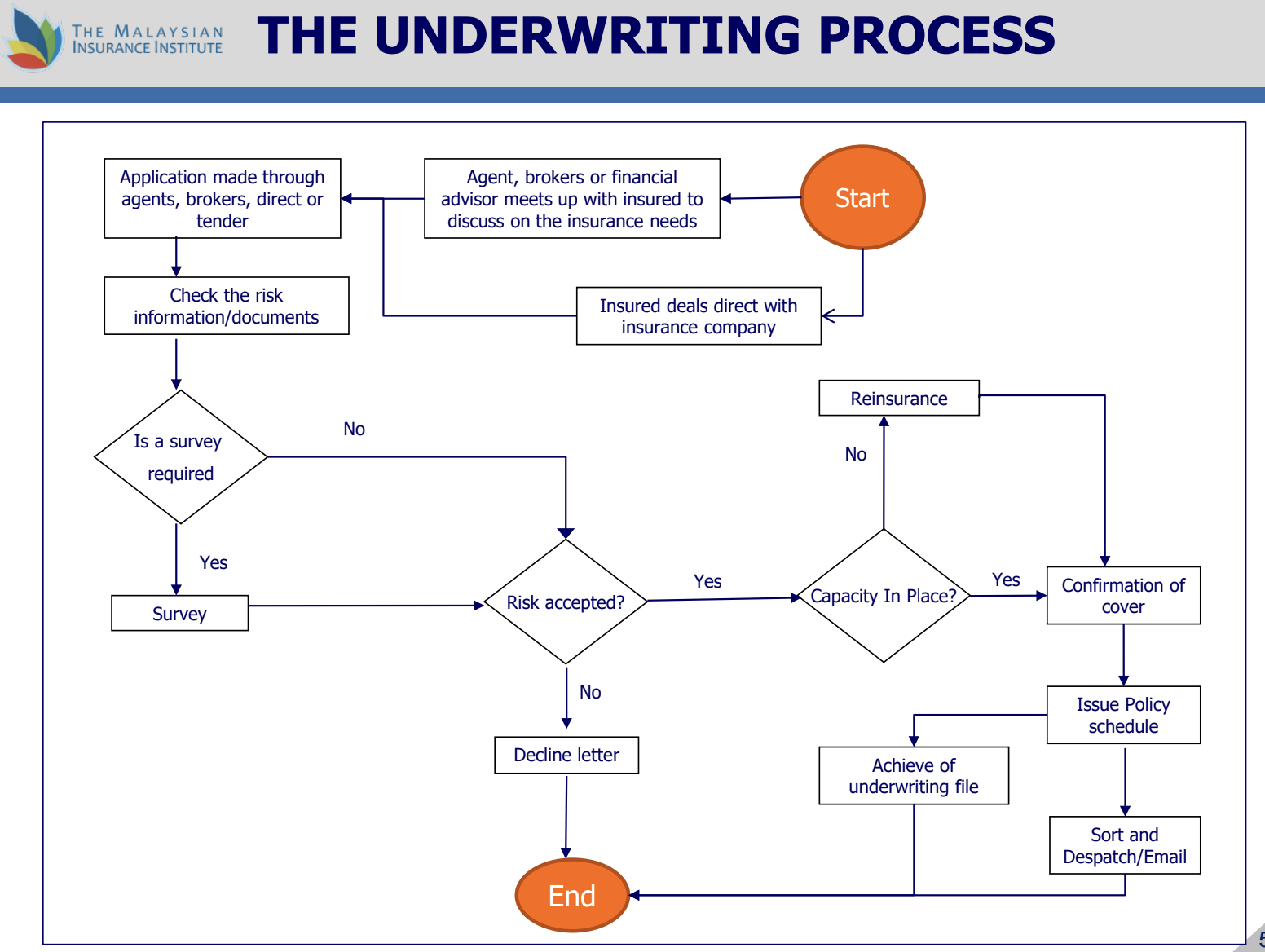

3. Underwriting Process

Although the process is really complicated in real life (which honestly frustrates agents and insured alike), the map above has simplified the underwriting process.

My Top 3 Learnings of Claims Management

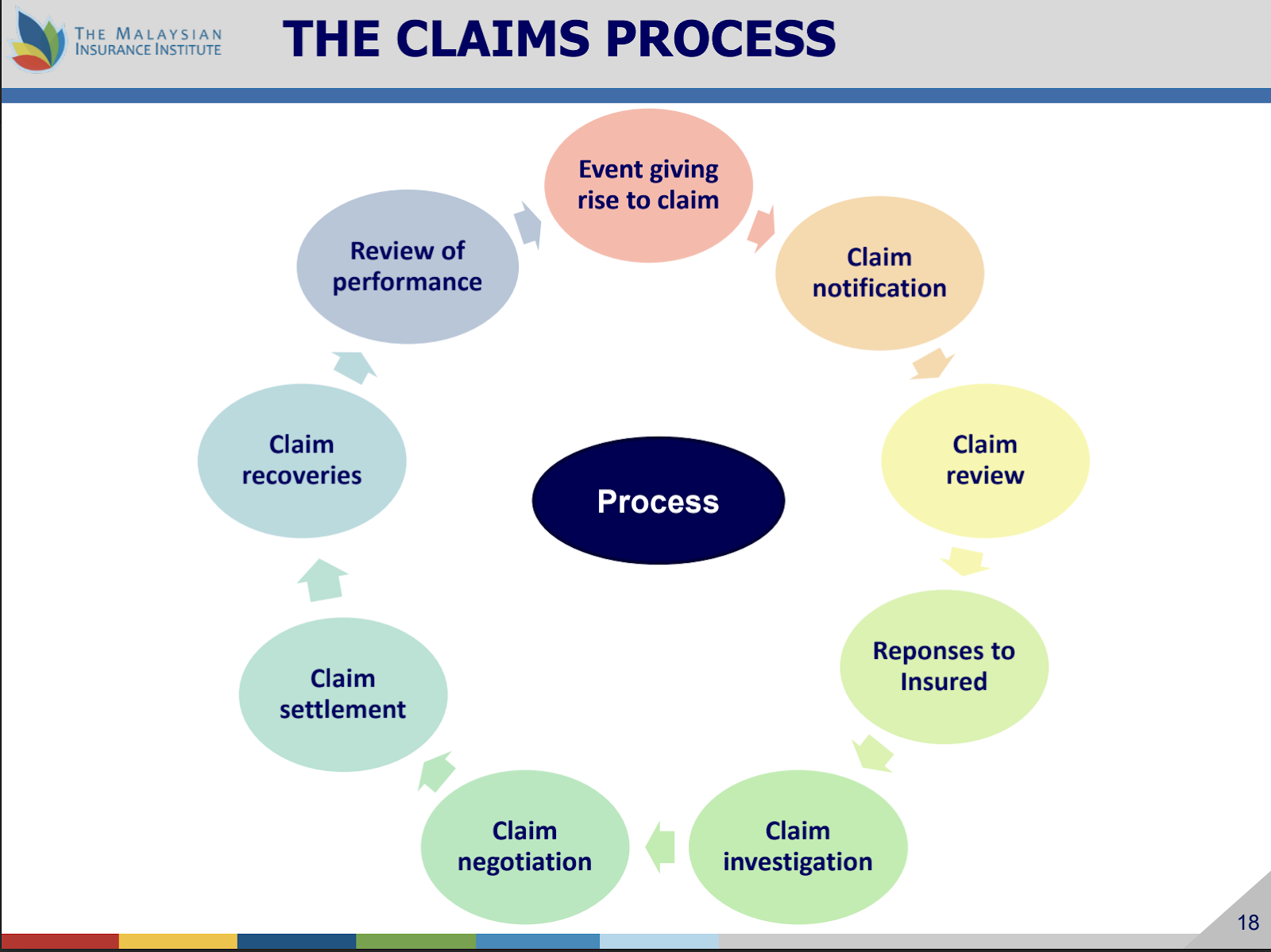

1. The Claims Process

When an event that was covered in the policy occur, the insurer must fulfil their contractual obligations by paying claims and fostering trust in the insurance industry.

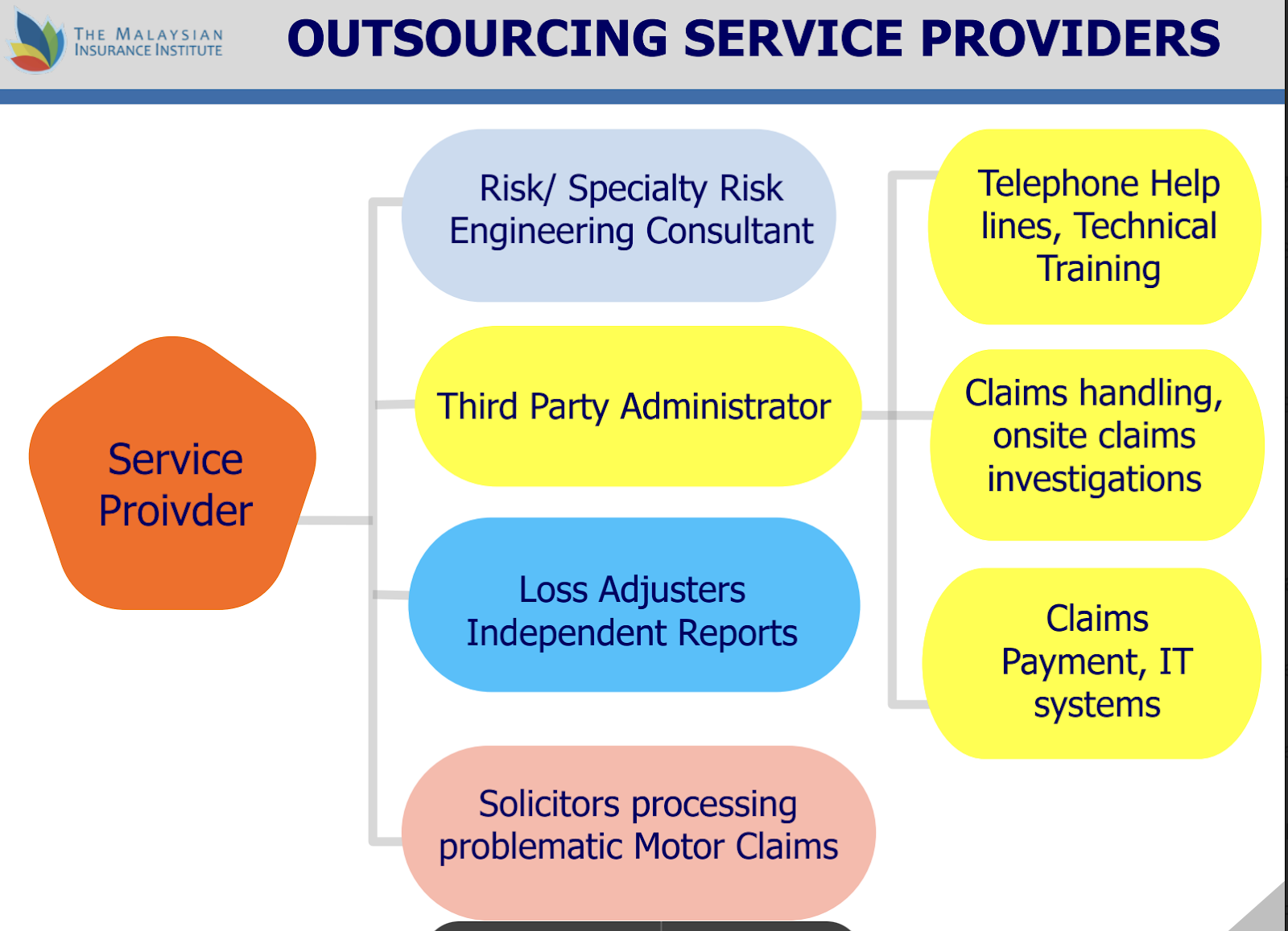

2. Outsourcing Service Providers

Outsourcing service providers in claims management offer specialized expertise and resources to insurance companies to efficiently handle various aspects of the claims process, such as claims intake, assessment, investigation, and settlement. These providers often leverage technology, data analytics, and industry knowledge to streamline operations, enhance customer experiences, and optimize costs for insurers, allowing them to focus on core business activities while ensuring timely and accurate claims resolution.

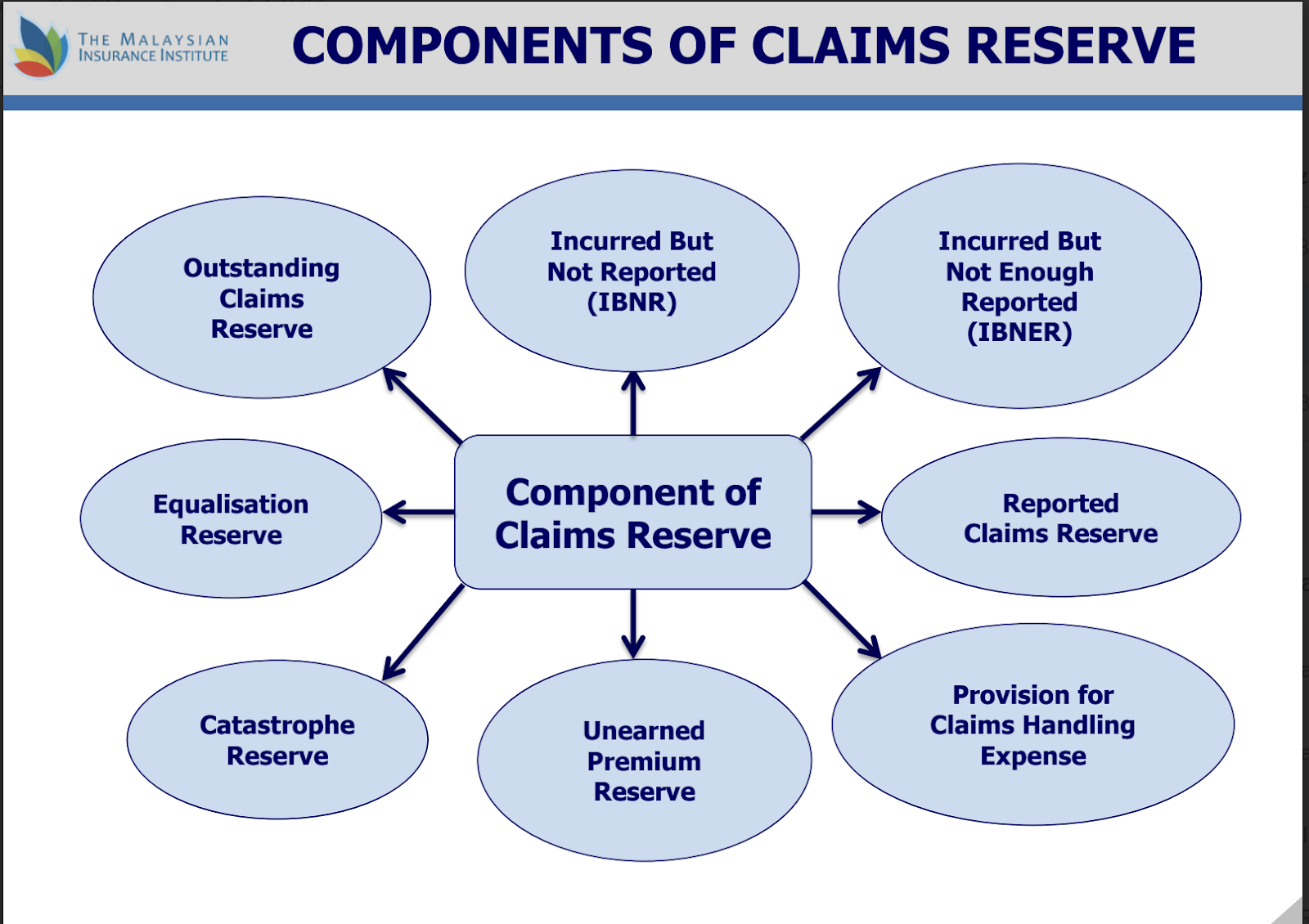

3. Components of Claims Reserve

By accurately estimating these components, insurers can ensure they have sufficient funds available to cover their liabilities and maintain financial stability while efficiently managing their claims portfolio.

Conclusion

I believe that I learnt a lot more from the 2 days of this intensive course than the learnings I provided above. Mr Kwong has more than 25 years of working experience in the industry and he broke down complex topics into easy digestible bits. I would definitely recommend this course to anyone who is new to the industry.